I canceled a subscription after 10 years. No email. No “sorry to see you go.” Nothing.

After a decade of paying them every month, I was just another canceled subscription in their system.

I get it. I’m probably lumped in with the thousands who sign up, use the app twice, and cancel within a month. Their data likely shows that most cancellations happen early, so why build systems to catch the long-timers?

But it made me think about how companies treat loyalty, and how quickly they forget the people who stick around.

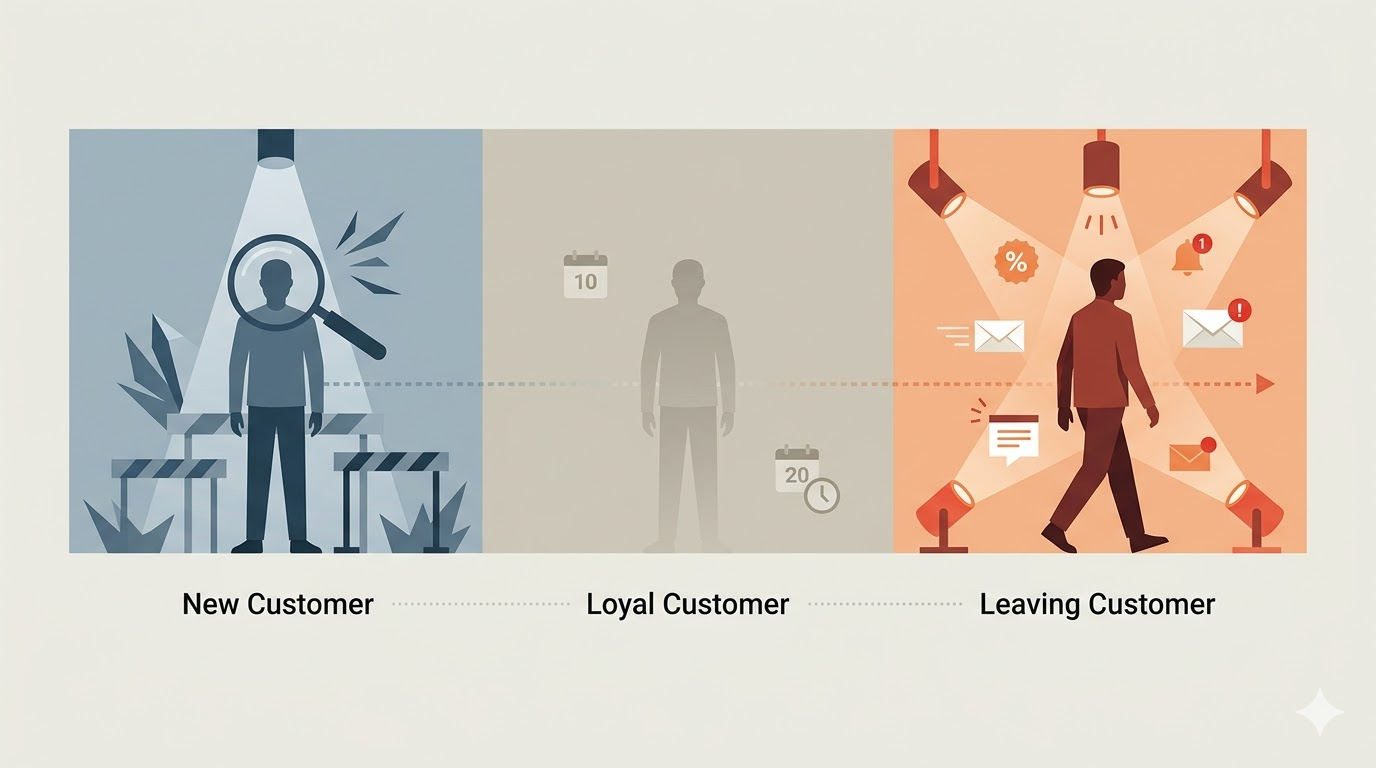

When You’re New, You’re a Risk

When I first moved to the US, Bank of America wouldn’t give me a regular credit card. No credit history. So they offered me a secured card: I put down $500, and I could spend up to that amount. I’d replenish it every couple of weeks, building credit slowly.

Months passed. Other banks gave me credit cards. Providian. American Express. Eventually, Bank of America did too, but by then I was bitter. I barely used it.

A few years later, I wanted to buy a house. Bank of America offered me a mortgage at something like 12% interest.

“You don’t have enough credit history.”

“You’re only here on a work visa. We don’t know if you’ll be here in three years.”

I got a mortgage from a smaller company at 5%.

Ten years later, I left Bank of America. Thirteen years after that, they’re still sending me offers to come back.

When You’re Loyal, You’re Invisible

My first car insurance in the US cost me $1,800 for six months. No credit history. No driver history here. That’s what I paid for the first two years before the premiums started to come down.

I stuck with that company for twenty years. The rates became reasonable, especially after bundling home and flood insurance.

Then, after twenty years, my car insurance premium jumped three or four times what it had been.

“New rules in Texas. It went up for everybody. There’s nothing we can do for you.”

I switched to another company. They offered me a rate that was one-sixth of what the old company wanted.

A year later, the old company started emailing me. They could offer me better rates now.

No, thanks.

The Pattern I Keep Seeing

When you’re new, you’re a risk. Companies make you prove yourself. They hedge. They charge more. They offer less.

When you’re loyal, you become invisible. You’re not a risk anymore, but you’re not a priority either. The systems optimize for acquiring new customers, not keeping the ones who stayed.

And when you leave? Suddenly, you’re valuable again. The offers come. The discounts appear. The attention returns.

I tried to cancel another service after three years. I’d used it twice, didn’t love it, and wanted to move on. Their website said I needed to email or send a letter to cancel. No phone number. No quick exit.

No “sorry to see you go” either.

What This Makes Me Wonder

I don’t expect companies to send me flowers when I cancel. But after 10 years with one, after 20 years with another, you’d think the systems would notice.

Maybe they do notice, and they’ve decided it’s not worth the effort. Maybe the math says that most people who cancel after that long won’t come back anyway, so why invest in retention at that point?

Or maybe the systems are just built to optimize for churn at the beginning and the end, while the middle, where loyalty lives, gets little attention.

I’m not angry about it. I’m just noticing it.

And I’m thinking about what it means for how we build things, how we treat people over time, and whether we’re designing systems that value the ones who stay.

Leave a Reply